Amine Kobeissi

AI & ML graduate student at Université de Montréal

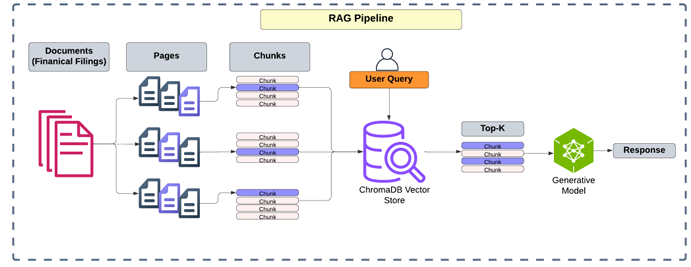

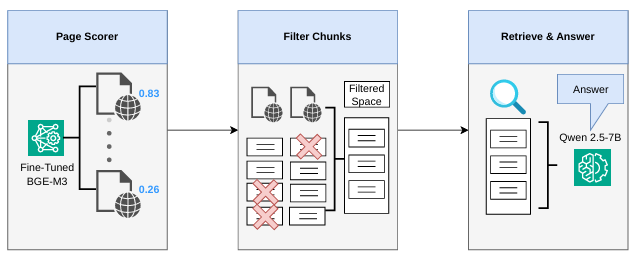

Hi, I’m Amine Kobeissi, a master’s student in computer science at Université de Montréal, where I focus on artificial intelligence and machine learning supervised by Prof. Philippe Langlais. My research interests lie at the intersection of machine learning, natural language processing, optimization, and quantitative finance. I’m currently focused on Retrieval-Augmented Generation (RAG) for financial question answering, studying how retrieval quality and advanced information-retrieval strategies affect downstream generation, and how to narrow the gap between ideal evidence and what systems actually retrieve.

I previously completed a B.Com. in Mathematics at McGill University with a concentration in business analytics, where I was a Research Fellow with Prof. Shoeb Hosain in the Data Sphere Lab.

This summer, I joined Morgan Stanley as a Quantitative Strategist Summer Associate on their eFX algo execution desk, and have several other data science internship experiences.

You can find more of my work on GitHub and connect with me on LinkedIn.

news

| May 22, 2026 |  My poster was accepted and I presented it at Journée de la recherche du DIRO 2026. You can click the image to view the poster, or open the presentation page. My poster was accepted and I presented it at Journée de la recherche du DIRO 2026. You can click the image to view the poster, or open the presentation page. |

|---|---|

| Apr 30, 2026 | My new paper, “Evaluating Retrieval in RAG Systems for Financial Question Answering over Long Documents”, has been accepted to CORIA-TALN 2026 in the main long paper track. The conference will take place in Nantes, France. |

| Apr 15, 2026 | Invited talk at the RALI seminar on my research on retrieval-augmented generation (RAG) for financial question answering systems. |

| Apr 07, 2026 |  I will be presenting my paper, “Measuring and Closing the Retrieval Gap in Financial Question Answering,” at the 39th Canadian Artificial Intelligence Conference in Vancouver (May 25–29, 2026), in the Graduate Student Track. You can click the image to view my CAIAC poster. I will be presenting my paper, “Measuring and Closing the Retrieval Gap in Financial Question Answering,” at the 39th Canadian Artificial Intelligence Conference in Vancouver (May 25–29, 2026), in the Graduate Student Track. You can click the image to view my CAIAC poster. |

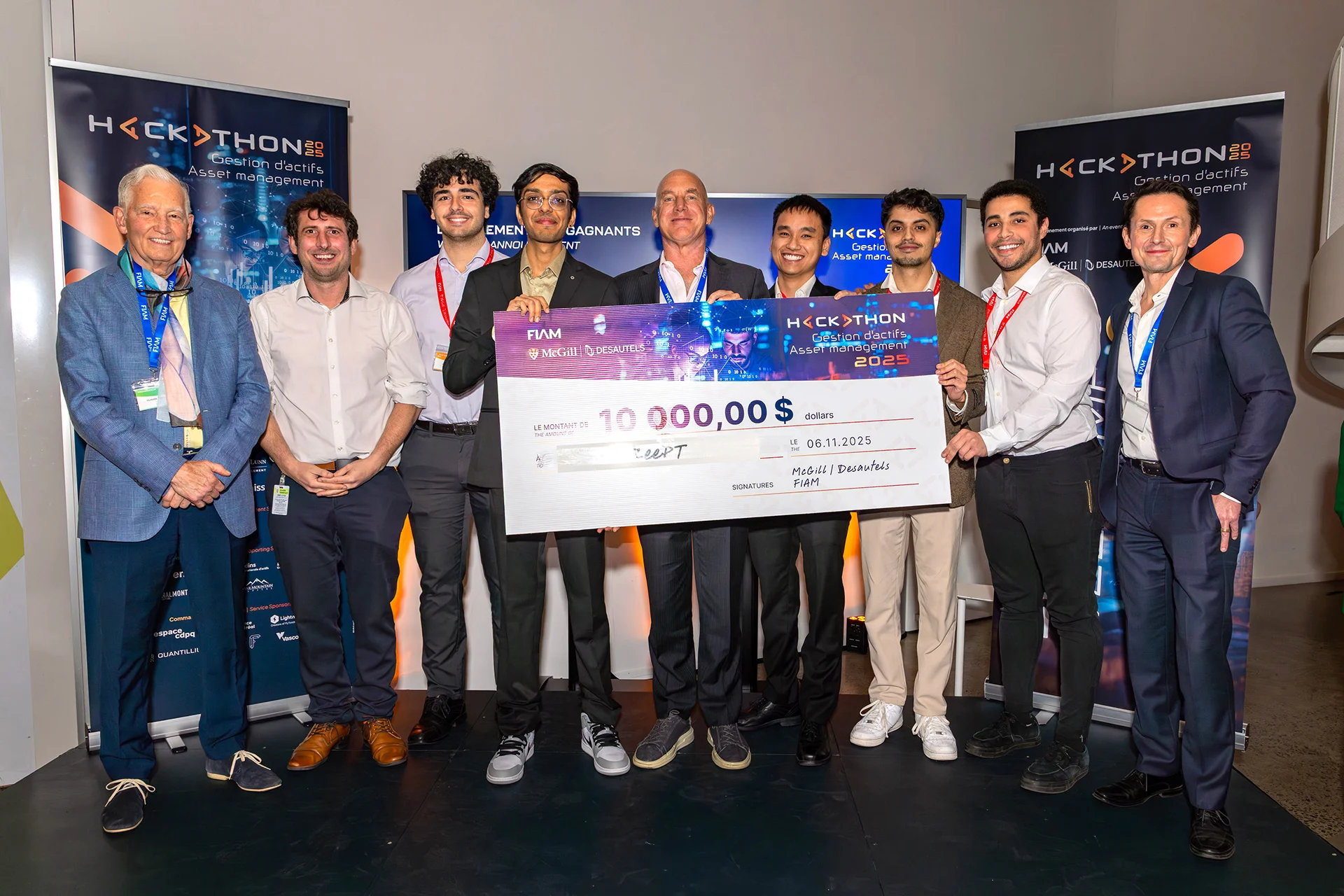

| Nov 06, 2025 |  My team and I won 2nd place in the 2025 FIAM Asset Management Hackathon! We built a systematic long–short equity strategy powered by reinforcement learning and deep learning to rebalance a portfolio over time. We also added an LLM agent that reads company filings and macroeconomic reports to help adjust the portfolio each month. My team and I won 2nd place in the 2025 FIAM Asset Management Hackathon! We built a systematic long–short equity strategy powered by reinforcement learning and deep learning to rebalance a portfolio over time. We also added an LLM agent that reads company filings and macroeconomic reports to help adjust the portfolio each month. |

selected publications

- Measuring and Closing the Retrieval Gap in Financial Question AnsweringIn Proceedings of the CAIAC 39th Edition, May 2026Accepted; Paper 175

- Evaluating Retrieval in RAG Systems for Financial Question Answering over Long DocumentsIn Proceedings of CORIA-TALN 2026, Jun 2026Accepted in the main long paper track